多因子模型搭建

1.引入之后需要用到的库

import tushare as ts # 股票基本数据相关库

import numpy as np # 科学计算相关库

import pandas as pd # 科学计算相关库

import talib # 股票衍生变量数据相关库

import matplotlib.pyplot as plt # 引入绘图相关库

from sklearn.ensemble import RandomForestClassifier # 引入分类决策树模型

from sklearn.metrics import accuracy_score # 引入准确度评分函数

import warnings

warnings.filterwarnings("ignore") # 忽略警告信息,警告非报错,不影响代码执行2.股票数据处理与衍生变量生成

# 1.股票基本数据获取

df = ts.get_k_data('000666',start='2015-01-01',end='2019-12-31')

df = df.set_index('date') # 设置日期为索引# 2.简单衍生变量构造

df['close-open'] = (df['close'] - df['open'])/df['open']

df['high-low'] = (df['high'] - df['low'])/df['low']df['pre_close'] = df['close'].shift(1) # 该列所有往下移一行形成昨日收盘价

df['price_change'] = df['close']-df['pre_close']

df['p_change'] = (df['close']-df['pre_close'])/df['pre_close']*100# 3.移动平均线相关数据构造

df['MA5'] = df['close'].rolling(5).mean()

df['MA10'] = df['close'].rolling(10).mean()

df.dropna(inplace=True) # 删除空值# 4.通过Ta_lib库构造衍生变量

df['RSI'] = talib.RSI(df['close'], timeperiod=12) # 相对强弱指标

df['MOM'] = talib.MOM(df['close'], timeperiod=5) # 动量指标

df['EMA12'] = talib.EMA(df['close'], timeperiod=12) # 12日指数移动平均线

df['EMA26'] = talib.EMA(df['close'], timeperiod=26) # 26日指数移动平均线

df['MACD'], df['MACDsignal'], df['MACDhist'] = talib.MACD(df['close'], fastperiod=12, slowperiod=26, signalperiod=9) # MACD值

df.dropna(inplace=True) # 删除空值# 查看此时的df后五行

df.tail()

3.特征变量和目标变量提取

X = df[['close', 'volume', 'close-open', 'MA5', 'MA10', 'high-low', 'RSI', 'MOM', 'EMA12', 'MACD', 'MACDsignal', 'MACDhist']]

y = np.where(df['price_change'].shift(-1)> 0, 1, -1)4.训练集和测试集数据划分

接下来,我们要将原始数据集进行分割,我们要注意到一点,训练集与测试集的划分要按照时间序列划分,而不是像之前利用train_test_split()函数进行划分。原因在于股票价格的变化趋势具有时间性,如果我们随机划分,则会破坏时间性特征,因为我们是根据当天数据来预测下一天的股价涨跌情况,而不是任意一天的股票数据来预测下一天的股价涨跌情况。 因此,我们将前90%的数据作为训练集,后10%的数据作为测试集,代码如下:

X_length = X.shape[0] # shape属性获取X的行数和列数,shape[0]即表示行数

split = int(X_length * 0.9)X_train, X_test = X[:split], X[split:]

y_train, y_test = y[:split], y[split:]5.模型搭建

model = RandomForestClassifier(max_depth=3, n_estimators=10, min_samples_leaf=10, random_state=1)

model.fit(X_train, y_train)模型使用与评估

1.预测下一天的涨跌情况

y_pred = model.predict(X_test)

print(y_pred)

a = pd.DataFrame() # 创建一个空DataFrame

a['预测值'] = list(y_pred)

a['实际值'] = list(y_test)

a.head()

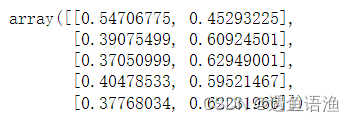

# 查看预测概率

y_pred_proba = model.predict_proba(X_test)

y_pred_proba[0:5]

2.模型准确度评估

from sklearn.metrics import accuracy_score

score = accuracy_score(y_pred, y_test)

print(score)![]()

# 此外,我们还可以通过模型自带的score()函数记性打分,代码如下:

model.score(X_test, y_test) ![]()

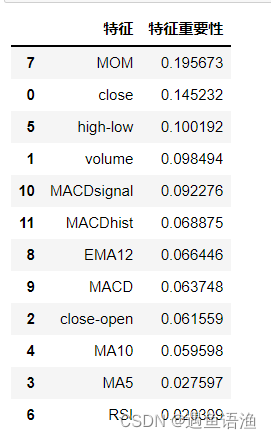

3.分析数据特征的重要性

model.feature_importances_

# 通过如下代码可以更好的展示特征及其特征重要性:

features = X.columns

importances = model.feature_importances_

a = pd.DataFrame()

a['特征'] = features

a['特征重要性'] = importances

a = a.sort_values('特征重要性', ascending=False)

a