1 加载数据

导入模块

import pandas as pd

from sklearn.metrics import roc_auc_score,roc_curve,auc

from sklearn.model_selection import train_test_split

from sklearn.linear_model import LogisticRegression

import numpy as np

import math

import xgboost as xgb

import toad

from toad.plot import bin_plot, badrate_plot

from matplotlib import pyplot as plt

from sklearn.preprocessing import StandardScaler

from toad.metrics import KS, F1, AUC

from toad.scorecard import ScoreCard

加载数据

# 加载数据

df = pd.read_csv('scorecard.txt')

print(df.info())

df.head()

df.describe()

数据划分

feature_list = list(df.columns)

feature_drop = ['bad_ind','uid','samp_type']

for lt in feature_drop:feature_list.remove(lt)

df_dev = df[df['samp_type']=='dev']

df_val = df[df['samp_type']=='val']

df_off = df[df['samp_type']=='off']

print(feature_list)

print('dev',df_dev.shape)

print('val',df_val.shape)

print('off',df_off.shape)

简单数据分析

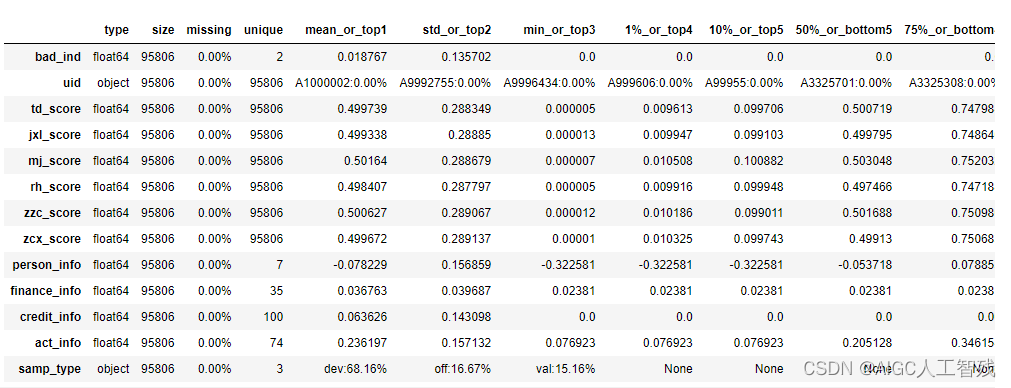

toad.detector.detect(df)

toad库能够同时处理数值型数据和分类型数据。由于没有缺失值,我们不用进行数据填充。

2 特征筛选

使用缺失率、IV和相关系数进行特征筛选。

# 根据缺失值、IV和相关系数进行特征筛选

dev_slt, drop_slt = toad.selection.select(df_dev, df_dev['bad_ind'], empty=0.7, iv=0.03, corr=0.7, return_drop=True, exclude=feature_drop)

print('keep:', dev_slt.shape,';drop empty:',drop_slt['empty'].shape,';drop iv:',drop_slt['iv'].shape,';drop_corr:',drop_slt['corr'].shape)

keep: (65304, 12) ;drop empty: (0,) ;drop iv: (1,) ;drop_corr: (0,)

3 卡方分箱

使用toad库,能够对所有特征切分节点,然后进行分箱

# 使用卡方分箱

# 使用卡方分箱

cmb = toad.transform.Combiner()

cmb.fit(dev_slt, dev_slt['bad_ind'], method='chi', min_samples=0.05, exclude=feature_drop)

bins = cmb.export()

print(bins)

{‘td_score’: [0.7989831262724624], ‘jxl_score’: [0.4197048501965005], ‘mj_score’: [0.3615303943747963], ‘zzc_score’: [0.4469861520889339], ‘zcx_score’: [0.7007847486465795], ‘person_info’: [-0.2610139784946237, -0.1286774193548387, -0.0537175627240143, 0.013863440860215, 0.0626602150537634, 0.078853046594982], ‘finance_info’: [0.0476190476190476], ‘credit_info’: [0.02, 0.04, 0.11], ‘act_info’: [0.1153846153846154, 0.141025641025641, 0.1666666666666666, 0.2051282051282051, 0.2692307692307692, 0.358974358974359, 0.3974358974358974, 0.5256410256410257]}

调整分箱

绘制Bivar图,观察该特征分享后是否单调性,不满足单调性需要调整分箱。

# 绘制bivar图,调整分箱

# 根据节点设置分箱

dev_slt2 = cmb.transform(dev_slt)

val2 = cmb.transform(df_val[dev_slt.columns])

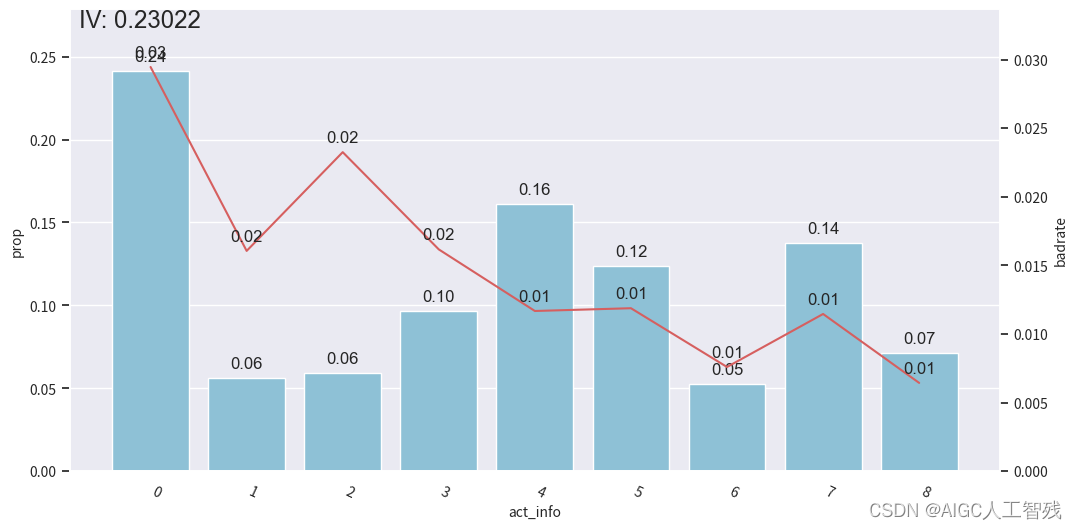

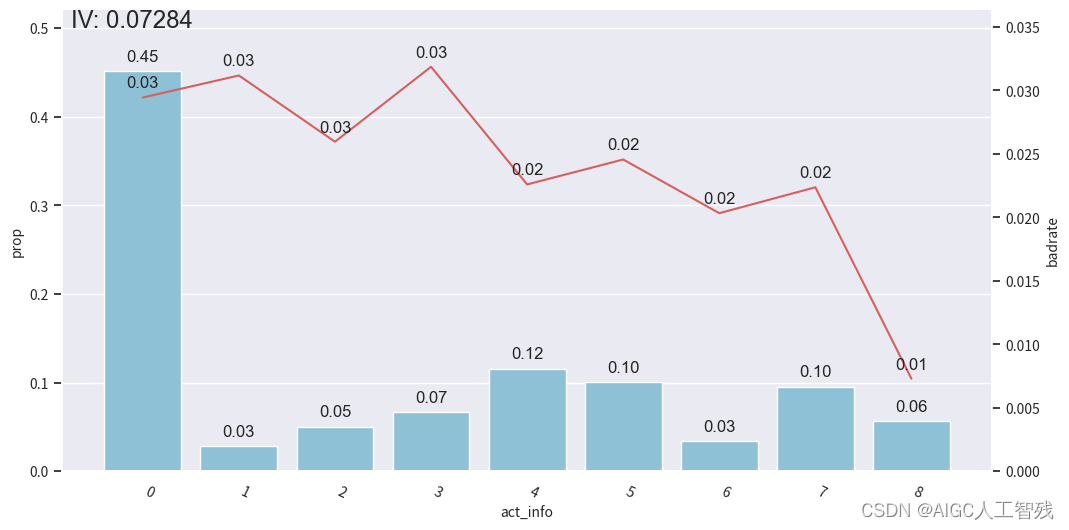

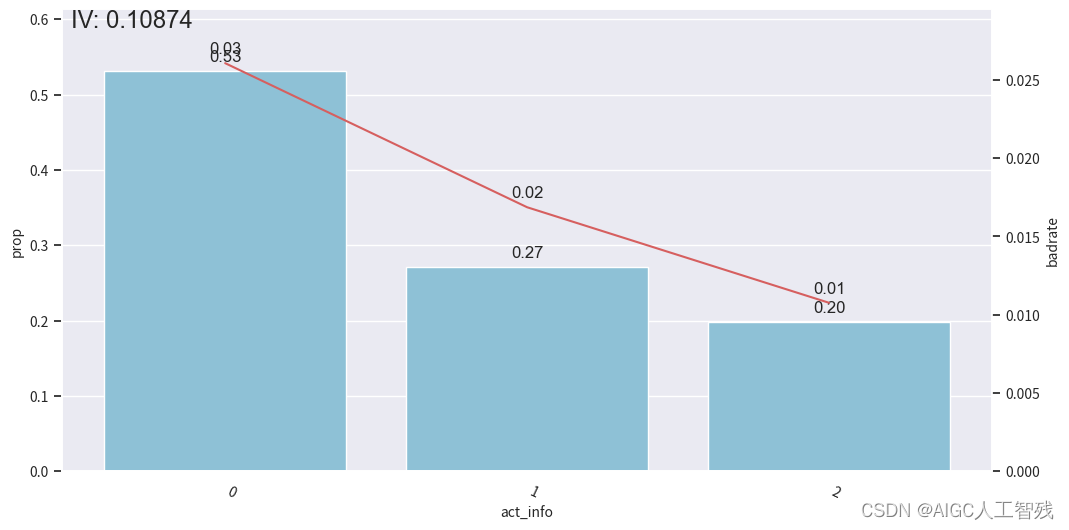

off2 = cmb.transform(df_off[dev_slt.columns])# 观察分箱后的图像-act_info

bin_plot(dev_slt2, x='act_info', target='bad_ind')

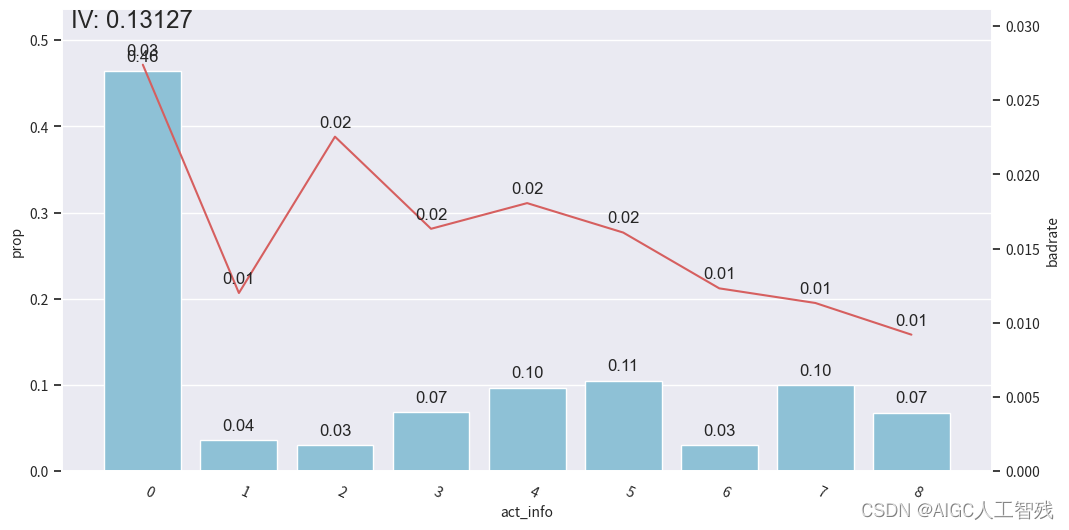

bin_plot(val2, x='act_info', target='bad_ind')

bin_plot(off2, x='act_info', target='bad_ind')

开发样本

测试样本

验证样本

我们能看到前3箱出现上下波动,与整体的单调递减趋势不符,所以进行分箱合并。

# 没有呈现单调性,需要进行合并

bins['act_info']

[0.1153846153846154,

0.141025641025641,

0.1666666666666666,

0.2051282051282051,

0.2692307692307692,

0.358974358974359,

0.3974358974358974,

0.5256410256410257]

将其调整为3个分箱

adj_bins = {'act_info':[0.1666666666666666,0.358974358974359]}

cmb.set_rules(adj_bins)dev_slt3 = cmb.transform(dev_slt)

val3 = cmb.transform(df_val[dev_slt.columns])

off3 = cmb.transform(df_off[dev_slt.columns])# 观察分箱后的图像

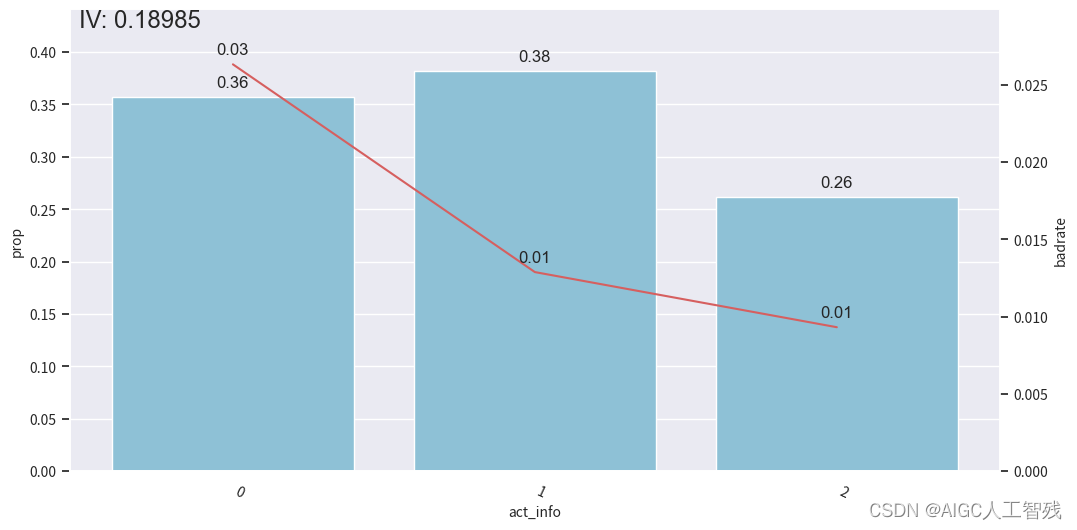

bin_plot(dev_slt3, x='act_info', target='bad_ind')

bin_plot(val3, x='act_info', target='bad_ind')

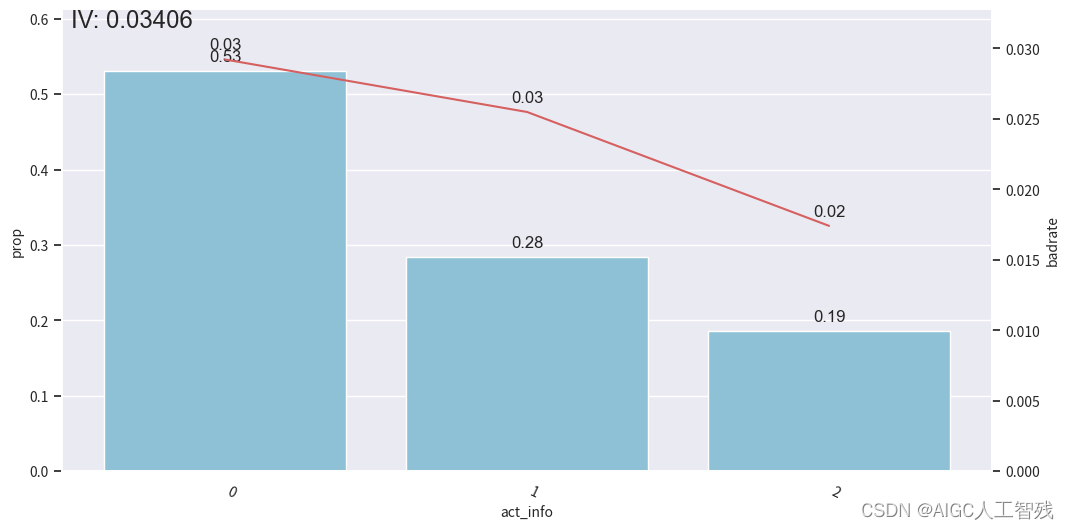

bin_plot(off3, x='act_info', target='bad_ind')

开发样本

测试样本

验证样本

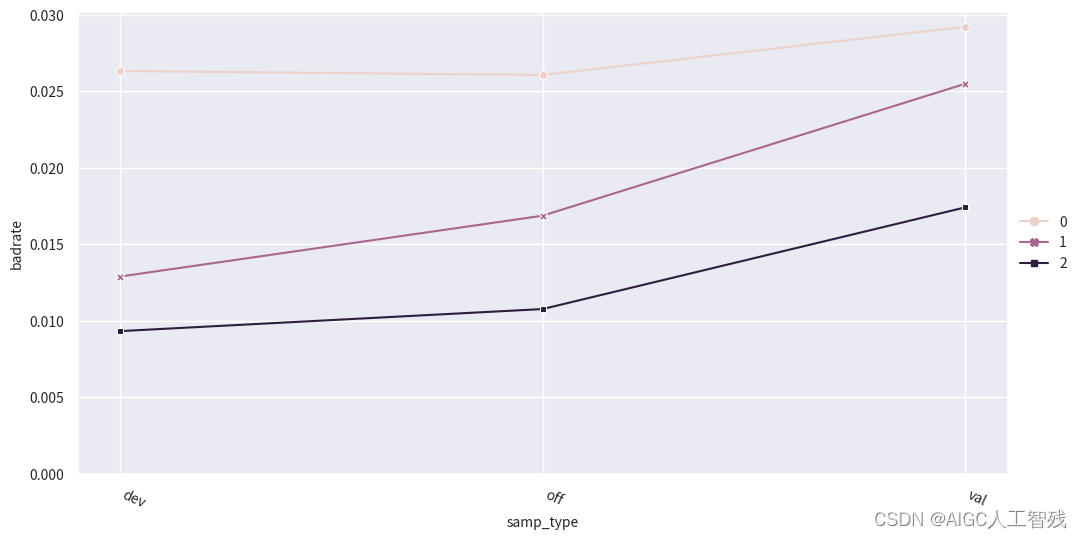

查看负样本占比关联图

# 绘制负样本占比关联图

data = pd.concat([dev_slt3, val3, off3], join='inner')

badrate_plot(data, x='samp_type', target='bad_ind', by='act_info')

其他特征分箱

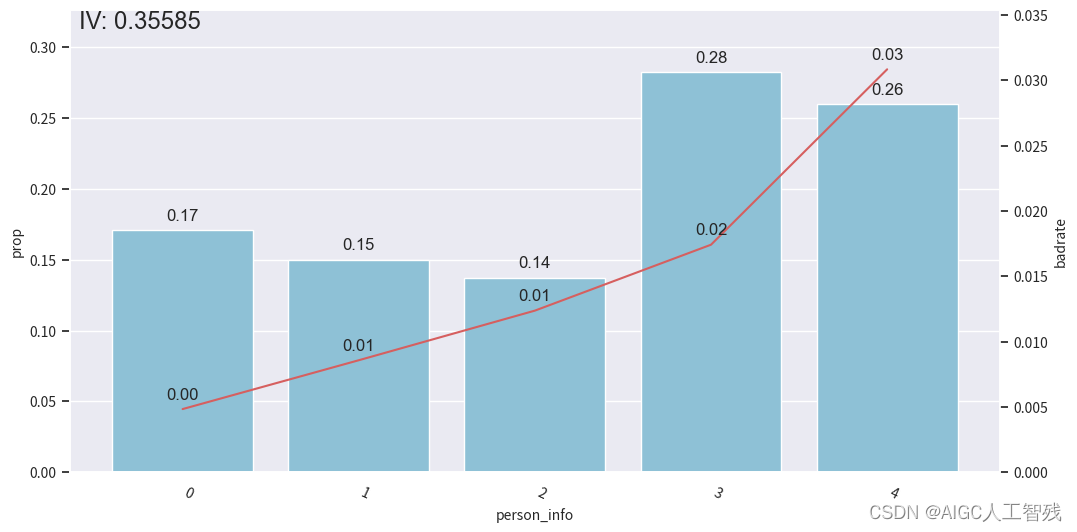

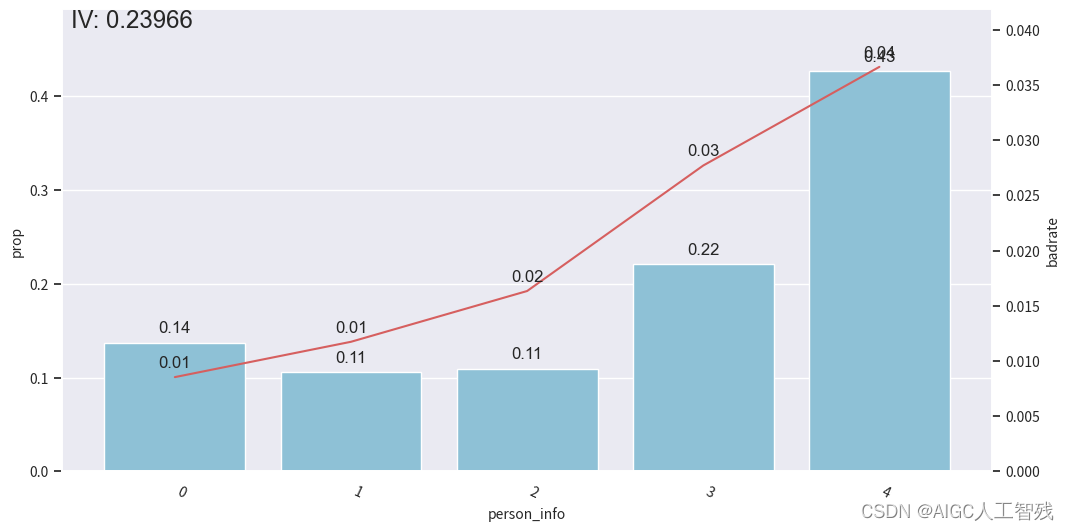

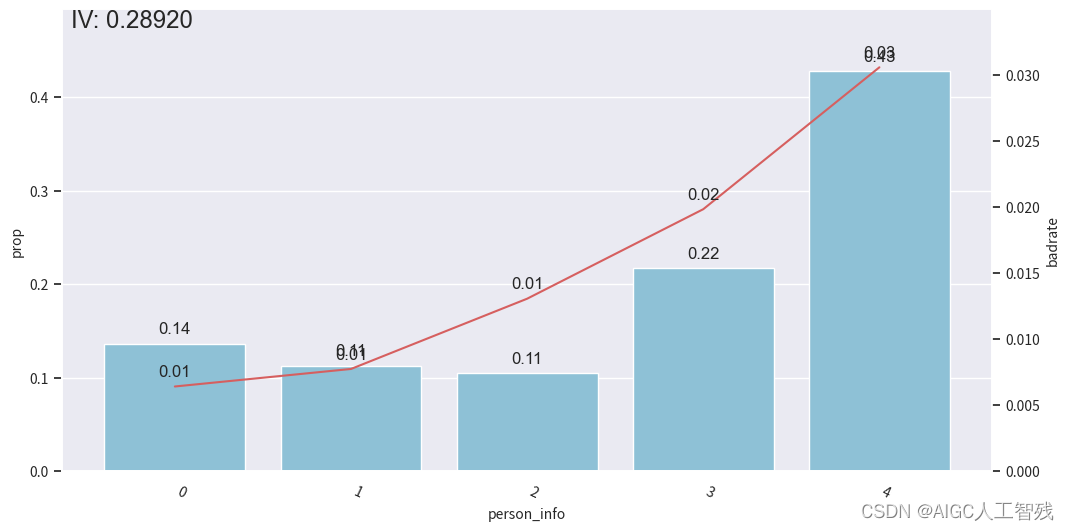

person_info特征分箱

bins['person_info']

[-0.2610139784946237,

-0.1286774193548387,

-0.0537175627240143,

0.013863440860215,

0.0626602150537634,

0.078853046594982]

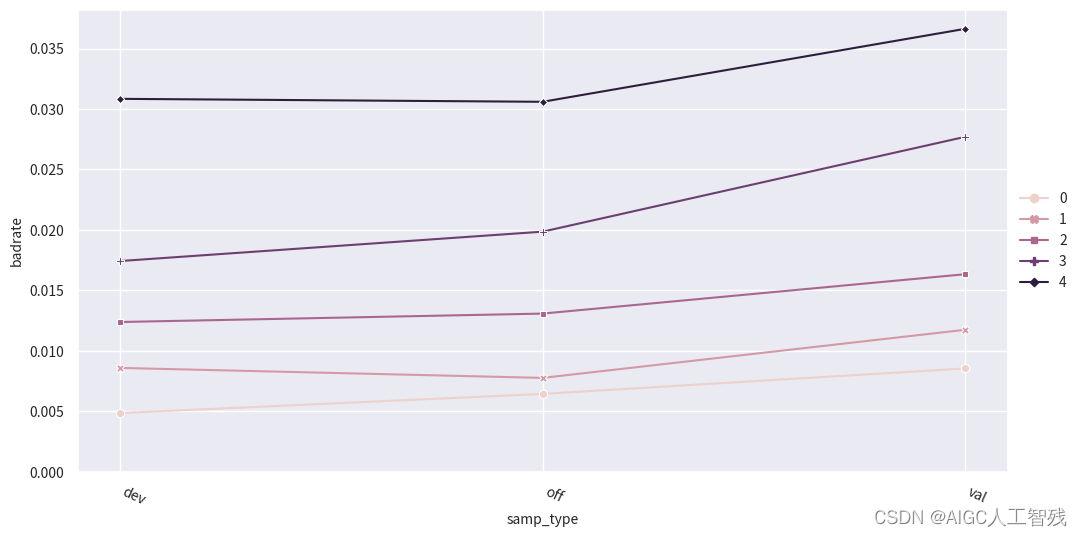

adj_bins = {'person_info':[-0.2610139784946237,-0.1286774193548387,-0.0537175627240143,0.078853046594982]}

cmb.set_rules(adj_bins)dev_slt3 = cmb.transform(dev_slt)

val3 = cmb.transform(df_val[dev_slt.columns])

off3 = cmb.transform(df_off[dev_slt.columns])data = pd.concat([dev_slt3, val3, off3], join='inner')

badrate_plot(data, x='samp_type', target='bad_ind', by='person_info')

# 观察分箱后的图像

bin_plot(dev_slt3, x='person_info', target='bad_ind')

bin_plot(val3, x='person_info', target='bad_ind')

bin_plot(off3, x='person_info', target='bad_ind')

bins['person_info']

负样本占比关联图

开发样本

测试样本

验证样本

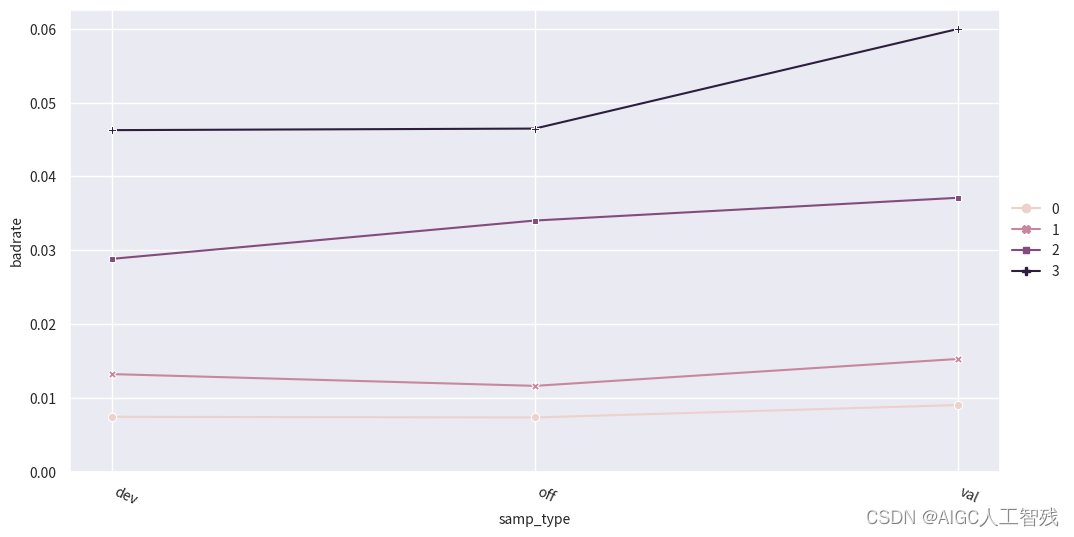

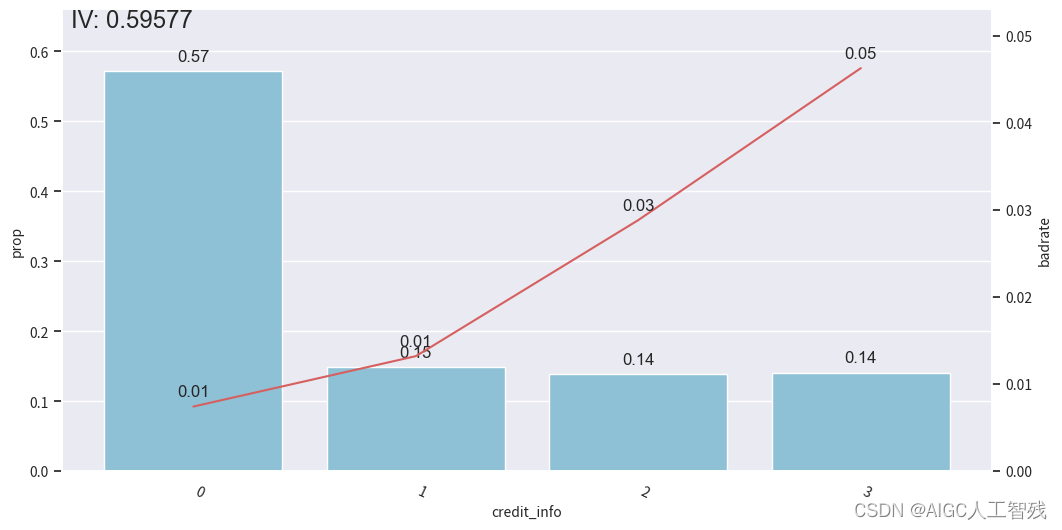

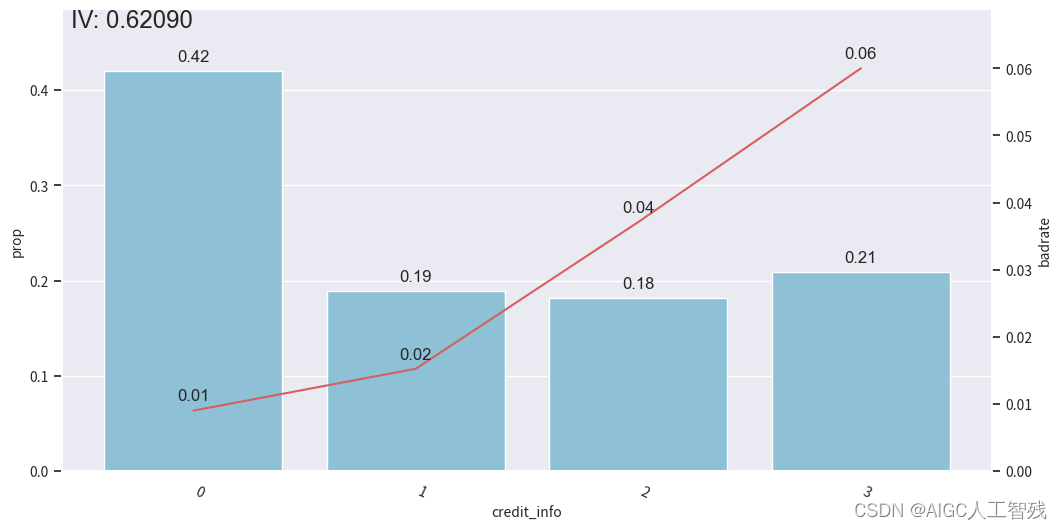

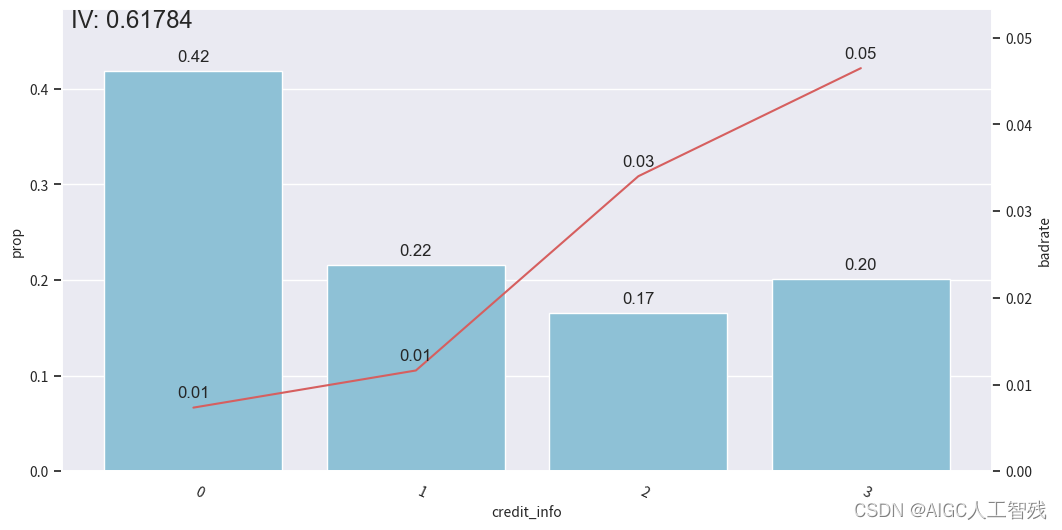

credit_info特征

# credit_info

badrate_plot(data, x='samp_type', target='bad_ind', by='credit_info')# 观察分箱后的图像

bin_plot(dev_slt3, x='credit_info', target='bad_ind')

bin_plot(val3, x='credit_info', target='bad_ind')

bin_plot(off3, x='credit_info', target='bad_ind')

bins['credit_info']

负样本占比

开发样本

测试样本

验证样本

其他特征分箱分为两个,所以不需要单独看。

4 WOE编码,并验证IV

# WOE编码,验证IV

woet = toad.transform.WOETransformer()

dev_woe = woet.fit_transform(dev_slt3, dev_slt3['bad_ind'], exclude=feature_drop)

val_woe = woet.transform(val3[dev_slt3.columns])

off_woe = woet.transform(off3[dev_slt3.columns])

data_woe = pd.concat([dev_woe, val_woe,off_woe])

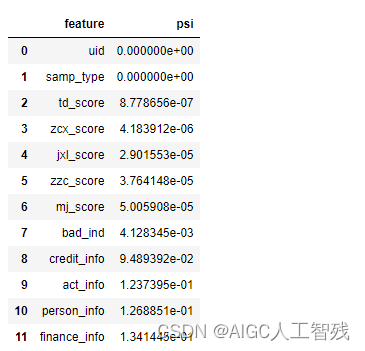

# 计算PSI

psi_df = toad.metrics.PSI(dev_woe,val_woe).sort_values(0)

psi_df = psi_df.reset_index()

psi_df = psi_df.rename(columns={'index':'feature', 0:'psi'})

psi_df

一般删除psi大于0.1的特征,但我们这里调整为0.13。

psi_013 = list(psi_df[psi_df.psi<0.13].feature)

# psi_013.extend(feature_drop)

data_psi = data_woe[psi_013]

dev_woe_psi = dev_woe[psi_013]

val_woe_psi = val_woe[psi_013]

off_woe_psi = off_woe[psi_013]

print(data_psi.shape)

(95806, 11)

由于卡方分箱后部分变量的IV降低,且整体相关程度增大,需要再次筛选特征。

dev_woe_psi2,drop_lst = toad.selection.select(dev_woe_psi, dev_woe_psi['bad_ind'], empty=0.6, iv=0.001, corr=0.5, return_drop=True, exclude=feature_drop)

print('keep:',dev_woe_psi2.shape,';drop empty:',drop_lst['empty'].shape,';drop iv:',drop_lst['iv'].shape,';drop corr:',drop_lst['corr'].shape)

keep: (65304, 7) ;drop empty: (0,) ;drop iv: (4,) ;drop corr: (0,)

5 再次特征筛选

使用逐步回归进行特征筛选,这里为线性回归模型,并选择KS作为评价指标。

# 特征筛选,使用逐步回归法进行筛选

dev_woe_psi_stp = toad.selection.stepwise(dev_woe_psi2,dev_woe_psi2['bad_ind'],exclude=feature_drop,direction='both',criterion='ks',estimator='ols',intercept=False)

val_woe_psi_stp = val_woe_psi[dev_woe_psi_stp.columns]

off_woe_psi_stp = off_woe_psi[dev_woe_psi_stp.columns]

data_woe_psi_std = pd.concat([dev_woe_psi_stp, val_woe_psi_stp, off_woe_psi_stp])

print(data_woe_psi_std.shape)

print(data_woe_psi_std.columns)

(95806, 6)

Index([‘uid’, ‘samp_type’, ‘bad_ind’, ‘credit_info’, ‘act_info’,

‘person_info’],

dtype=‘object’)

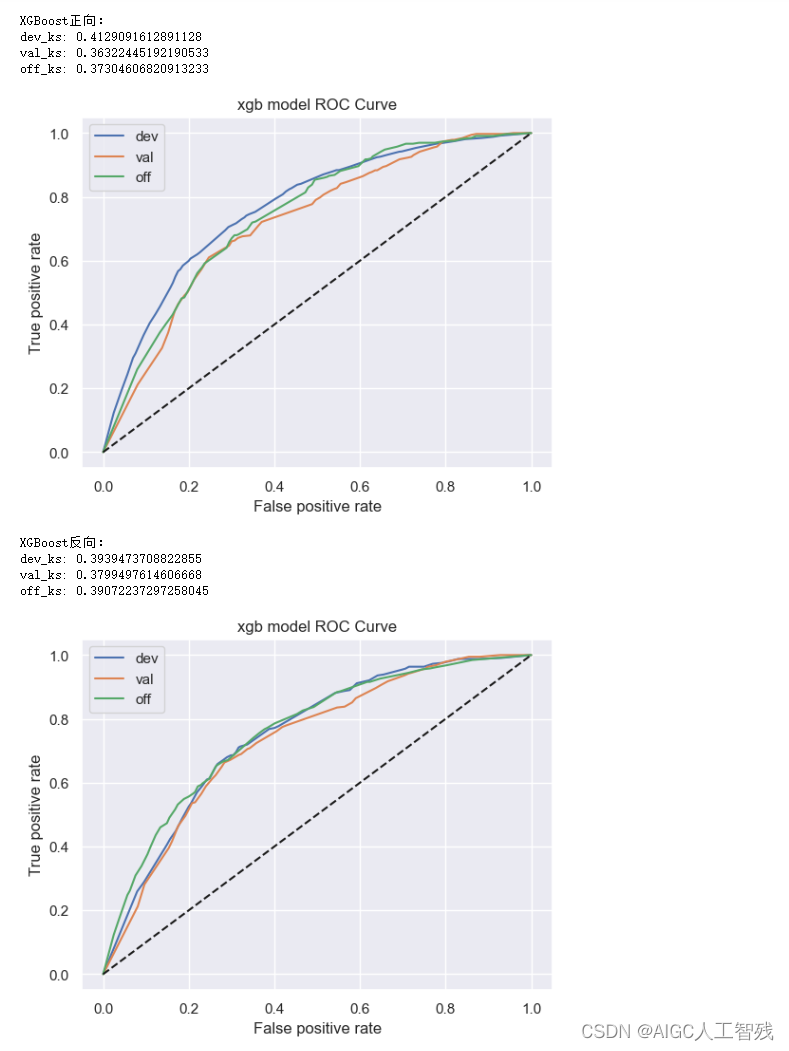

6 模型训练

定义逻辑回归模型和XGBoost模型的函数

# 进行模型训练

def lr_model(x,y,valx,valy,offx,offy,c):model = LogisticRegression(C=c, class_weight='balanced')model.fit(x,y)# devy_pred = model.predict_proba(x)[:,1]fpr_dev, tpr_dev, _ = roc_curve(y,y_pred)dev_ks = abs(fpr_dev-tpr_dev).max()print('dev_ks:',dev_ks)y_pred = model.predict_proba(valx)[:,1]fpr_val, tpr_val, _ = roc_curve(valy,y_pred)val_ks = abs(fpr_val-tpr_val).max()print('val_ks:',val_ks)y_pred = model.predict_proba(offx)[:,1]fpr_off, tpr_off, _ = roc_curve(offy,y_pred)off_ks = abs(fpr_off-tpr_off).max()print('off_ks:',off_ks)plt.plot(fpr_dev, tpr_dev, label='dev')plt.plot(fpr_val, tpr_val, label='val')plt.plot(fpr_off, tpr_off, label='off')plt.plot([0,1],[0,1],'k--')plt.xlabel('False positive rate')plt.ylabel('True positive rate')plt.title('lr model ROC Curve')plt.legend(loc='best')plt.show()# xgb模型

def xgb_model(x,y,valx,valy,offx,offy):model = xgb.XGBClassifier(learning_rate=0.05,n_estimators=400,max_depth=2,min_child_weight = 1,subsample=1,nthread=-1,scale_pos_weight=1,random_state=1,n_jobs=-1,reg_lambda=300)model.fit(x,y)# devy_pred = model.predict_proba(x)[:,1]fpr_dev, tpr_dev, _ = roc_curve(y,y_pred)dev_ks = abs(fpr_dev-tpr_dev).max()print('dev_ks:',dev_ks)y_pred = model.predict_proba(valx)[:,1]fpr_val, tpr_val, _ = roc_curve(valy,y_pred)val_ks = abs(fpr_val-tpr_val).max()print('val_ks:',val_ks)y_pred = model.predict_proba(offx)[:,1]fpr_off, tpr_off, _ = roc_curve(offy,y_pred)off_ks = abs(fpr_off-tpr_off).max()print('off_ks:',off_ks)plt.plot(fpr_dev, tpr_dev, label='dev')plt.plot(fpr_val, tpr_val, label='val')plt.plot(fpr_off, tpr_off, label='off')plt.plot([0,1],[0,1],'k--')plt.xlabel('False positive rate')plt.ylabel('True positive rate')plt.title('xgb model ROC Curve')plt.legend(loc='best')plt.show()

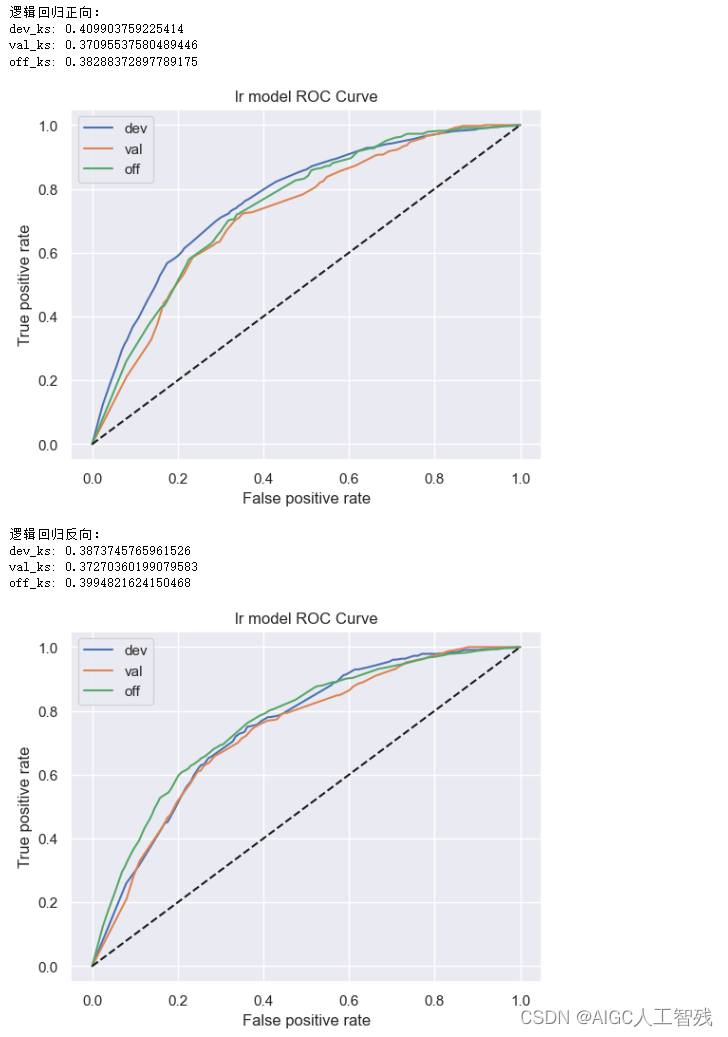

定义模型函数的使用函数,在函数中分别进行正向调用和逆向调用,验证模型的效果上限。如逆向模型训练集KS值明显小于正向模型训练集KS值,说明当前时间外样本分布与开发样本差异较大,需要重新划分样本集。

start_train(data_woe_psi_std,target='bad_ind', exclude=feature_drop)

- XGBoost的效果没有好于逻辑回归模型,因此特征不需要进行再组合;

- 反向lr模型的结果没有显著好于正向调用的结果,因此该模型在当前特征空间下没有优化的空间;

- lr正向训练和反向训练的ks值在5%以内,所以不需要调整时间稳定性较差的变量。

计算训练集、测试集和验证集的ks、F1和auc值

7 计算指标评估模型,生成模型报告

# 分别计算ks,F1和auc值

target = 'bad_ind'

lt = list(data_woe_psi_std.columns)

for i in feature_drop:lt.remove(i)devv = data_woe_psi_std[data_woe_psi_std['samp_type']=='dev']

vall = data_woe_psi_std[data_woe_psi_std['samp_type']=='val']

offf = data_woe_psi_std[data_woe_psi_std['samp_type']=='off']

x,y=devv[lt], devv[target]

valx,valy = vall[lt],vall[target]

offx,offy = offf[lt], offf[target]

lr = LogisticRegression()

lr.fit(x,y)prob_dev = lr.predict_proba(x)[:,1]

print('训练集')

print('F1:',F1(prob_dev,y))

print('KS:',KS(prob_dev,y))

print('AUC:',AUC(prob_dev,y))prob_val = lr.predict_proba(valx)[:,1]

print('测试集')

print('F1:',F1(prob_val,valy))

print('KS:',KS(prob_val,valy))

print('AUC:',AUC(prob_val,valy))prob_off = lr.predict_proba(offx)[:,1]

print('验证集')

print('F1:',F1(prob_off,offy))

print('KS:',KS(prob_off,offy))

print('AUC:',AUC(prob_off,offy))# 验证集的模型PSI和特征PSI

print('模型PSI:', toad.metrics.PSI(prob_dev,prob_off))

print('特征PSI:\n', toad.metrics.PSI(x,offx).sort_values(0))

训练集

F1: 0.02962459026532253

KS: 0.40665138719594446

AUC: 0.7683462756870743

测试集

F1: 0.03395860284605433

KS: 0.3709553758048945

AUC: 0.723771920780572

验证集

F1: 0

KS: 0.38288372897789186

AUC: 0.7447410631197128

模型PSI: 0.3372146799079187

特征PSI:

credit_info 0.098585

act_info 0.124820

person_info 0.127210

dtype: float64

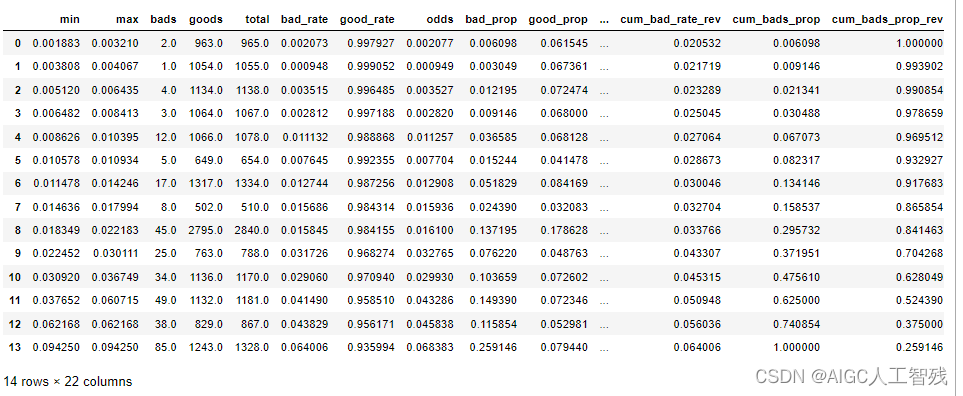

生成验证集的ks报告

toad.metrics.KS_bucket(prob_off, offy, bucket=15, method='quantile')

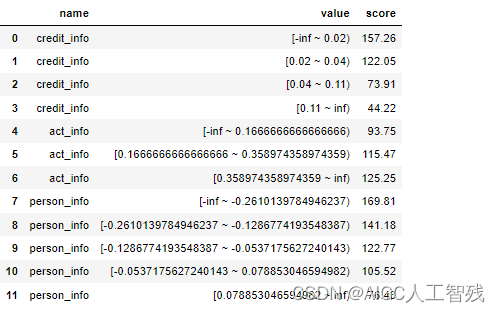

8 生成评分卡

# 用toad生成评分卡

card = ScoreCard(combiner=cmb,transer=woet, C=0.1,class_weight='balanced',base_score=600,base_odds=35,pdo=60,rate=2)

card.fit(x,y)

final_card = card.export(to_frame=True)

final_card

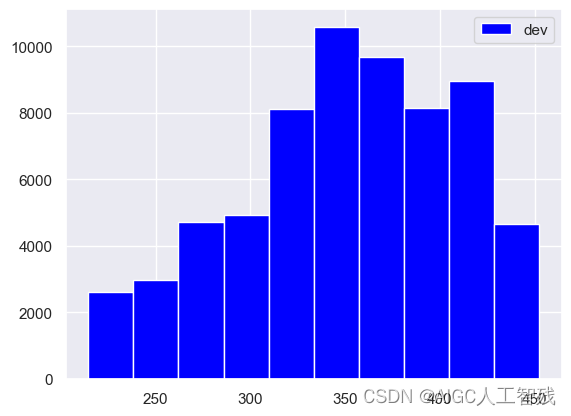

对训练集、测试集和验证集应用评分卡,预测用户的分数。这里要注意要传入原始数据,不要传入woe编码转化后和分箱后的数据。

# 评分卡进行预测

df_dev['score'] = card.predict(df_dev)

df_val['score'] = card.predict(df_val)

df_off['score'] = card.predict(df_off)

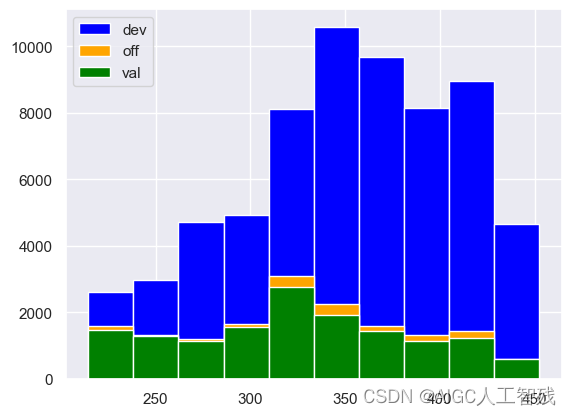

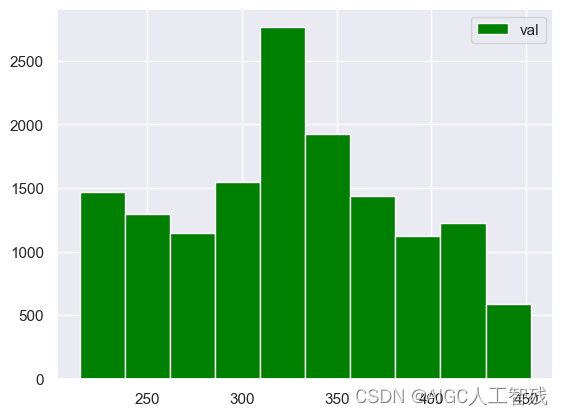

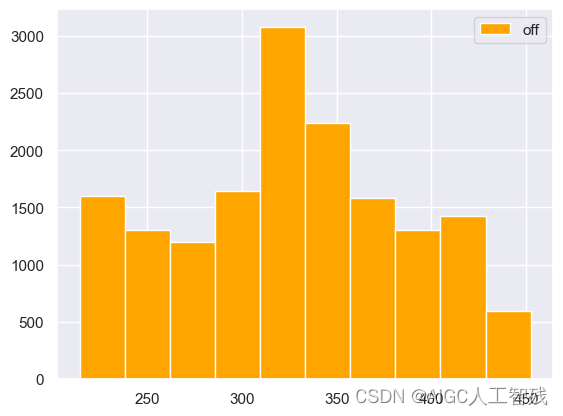

plt.hist(df_dev['score'], label = 'dev',color='blue', bins = 10)

plt.legend()

plt.hist(df_val['score'], label = 'val',color='green', bins = 10)

plt.legend()

plt.hist(df_off['score'], label = 'off',color='orange', bins = 10)

plt.legend()

三组评分数据在一个图中

plt.hist(df_dev['score'], label = 'dev',color='blue', bins = 10)

plt.hist(df_off['score'], label = 'off',color='orange', bins = 10)

plt.hist(df_val['score'], label = 'val',color='green', bins = 10)

plt.legend()